Water, Water, Everywhere

December 15, 2017 | By Ian McTeer

Although I did not shoot an albatross with my crossbow, I certainly felt a bit like Samuel Coleridge’s The Rime of the Ancient Mariner as I sloshed through my backyard this summer. “Water, water, everywhere/nor any drop to drink.”

I am fortunate in that my house is high and dry unlike many other buildings in Eastern Canada that experienced one of the rainiest summers in recent memory. Several low spots in my yard did not dry out until mid-July, and the mosquitoes, the little devils, had a banner year. On the other hand, British Columbia experienced a record forest fire season. My brother-in-law had to flee his home in Vancouver because the city was blanketed with smoke from forest fires burning in the interior. His lung ailment combined with smoky air made his life so miserable that he joined us in Apple Hill, ON, happily sloshing around in our backyard for several weeks; it reminded him of a “normal” Vancouver summer.

I spoke to an HVAC contractor friend of mine recently and he told me that he had a dozen requests from existing customers to move condensing units away from their houses, more this summer than ever before. Often contractors get this request because homeowners want to renovate or build extensions onto the house or to add a deck or patio. But no, in every case the condensers had to be moved because basement waterproofing crews needed to excavate around foundation walls in order to fix a basement flooding problem. Excessive rain likely combined with poor drainage from roof runoff (many municipalities no longer allow runoff to be directed to the storm sewer) caused extra hydraulic pressure against creaky old foundation walls incapable of withstanding this force of nature.

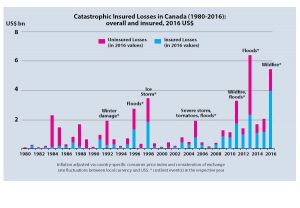

Source: 2017 Munich Re, Geo Risks Research, NatCatSERVICE. As of February 2017.

OVERLAND FLOODING

The Insurance Bureau of Canada (IBC) reported recently that, “water is the new fire” meaning that water damage is now the leading cause of insurer payouts for property damage. The IBC notes that since 2009, insurance companies have paid out an average of $400 million per year for claims related to severe weather events.

Blair Feltmate, a University of Waterloo professor, told Andrew Duffy of the Ottawa Citizen that “flooding, by a very large margin, is the greatest extreme weather event challenging Canada today – by far.” He also mentioned that the average homeowner in both Calgary, AB and Toronto, ON, both hit with serious flooding events in 2013, paid out an average of $42,000 each for repairs to flooded basements. In Ontario during August 2017, a severe thunderstorm dumped a record 290 mm. of rain onto Windsor, Tecumseh and other parts of Essex County flooding over 6,000 basements and causing an estimated $124 million in damage.

Overland flood insurance is available in Canada, but is typically not part of regular home insurance and not all insurers offer coverage. Premiums tend to be very expensive and may not cover 100 per cent of the damage, so most building owners tend to skip the coverage and take their chances. Homeowners can also face loss of coverage if they have failed to notify the insurer of “changes to the material risk” related to the insured property, such as a finishing the basement or installing a new furnace.

Insurers have increased deductibles too. For example, my sewer back-up endorsement deductible is now $5000. Plumbing contractors should offer the installation of an appropriate sewer backflow valve to every customer.

OVERLAND FLOOD MITIGATION

Once the roaring floodwater has subsided, the residual standing water is dangerous. It is a soup of sewage, toxic chemicals, petroleum, dead animals and debris such as sharp metal, broken glass and nail embedded wood. HVAC technicians helping flood ravaged customers must be aware of these dangers; wear CSA approved boots (green triangle minimum) and be sure your tetanus shot is up to date.

Technicians should not enter buildings until they are deemed safe by the local authorities. When faced with such terrible losses, some homeowners might inquire about making repairs to flooded equipment thinking they will save money on uninsured equipment that should be replaced.

Remember, the CSA B149.1-10 in Section 4.5, Suitability of Use, and paragraph 4.5.5 requires that an appliance that has been exposed to fire, explosion, flood, or other damage shall not be offered for sale, installed, re-activated or connected to the supply, without; (a) approval of the authority having jurisdiction; or (b) inspection and confirmation by a Gas Technician I or II (as appropriate for the appliance input rating) that it is fit for continued use.

Be sure to also consult the equipment manufacturer. Your manufacturer should have a service bulletin or technical article explaining how an appliance might be restored after a flooding event. Flood damaged components must not be claimed against a manufacturer’s warranty or extended warranty. In many cases of overland flooding, the HVAC equipment, including boilers, geo indoor units, oil/gas furnaces, air handlers, water heaters, accessories and even the ductwork, is replaced as required. Sometimes, if the flooding is not too severe, some equipment could be restored. For example, an otherwise undamaged condensing unit or heat pump outdoor unit could be cleaned provided the flood waters did not reach the compressor terminals or control compartment.

FRESH WATER FLOODING

I spent a few years working for the service department of a large HVAC service contractor in Toronto. When it came to loading my service truck with stock replacement items on my first day, the stock-keeper plopped a pair of Wellington rubber boots into the back of the truck.

“What are they for?” I asked. He said, “You’ll see.”

It wasn’t even a week later before I came across my first basement freshwater flood caused by a 40 gallon gas water heater rusting out its storage tank. The homeowner had no idea how to turn off the water, eventually calling the city to shut it off outside. Often, basements with a lot of clutter fill-up to swimming pool depth because, invariably, a piece of paper or rag floats over to the floor drain and blocks it allowing water to fill the basement. Or, even worse, the floor drain is blocked by tree roots. Sometimes the sump pump does not work. It was sitting there for 20 years without being tested and failed when needed.

FRESH WATER FLOOD MITIGATION

Freshwater floods caused by water heater leaks, T&P valve blow-offs, burst plumbing pipes, and improperly installed accessories such as humidifier water connections may be somewhat less serious than overland flooding because most homeowner insurance policies will cover such damage. Without coverage, it may be possible to restore some equipment (once again, consult the equipment manufacturer before proceeding) provided the work is done by a properly licensed and experienced technician.

A freshwater flooded furnace could be re-activated but the amount of time and material involved might be a limiting factor. For example, an entry level condensing furnace should have the following components replaced:

• All electrical safety components such as the primary and secondary limit controls, flame rollout switch(es) and pressure switches

• Gas valve

• Ignition control

• Combustion blower assembly

• Fan motor

Then,

• Soaked cabinet insulation must be replaced

• Gas burners and orifices must be cleaned or replaced

• Gas manifold cleared of water, gas piping checked for water at appliance dirt pocket

• All electrical connections must be completely dry and any damaged wiring replaced.

• Once repairs are completed, the furnace must be run tested including a test of all safety controls.

Consider whether all this, plus labour, is less than a new unit? On the other hand, in the case of a more sophisticated appliance it is actually less expensive to replace it than to repair it, in my view. The cost of a new ECM, multi-speed or variable speed draft inducer motor, main control board, inducer drive board, personality module, user interface, modulating gas valve and other electronic items makes replacement the only way to go for continued reliability. While a disaster for the homeowner, the HVAC contractor may be able to include an affordable upgrade to the existing insured system in some flood situations providing somewhat of a silver lining for the end-user.

HVAC AND WATER

What about minor flooding, just enough to cause property damage and really annoy the customer, even if it is their fault?

Did your company install a condensing gas furnace today? Then the installers worked with water. Installers must be concerned about where the condensed water vapour in the flue gas ends-up. Venting must be sloped according to the manufacturer’s instructions to be sure water does not collect in low spots, creating a blockage. Then, installers must create a path to an open/vented drain to handle the internally generated condensed water vapour.

If you did not do any or all of these things properly, then a breakdown generating a call-back is guaranteed or, even worse, property damage caused by flooding will see you in hot water.

MINOR FLOODING

A 100K Btuh gas-fired appliance will produce approximately two gallons (7.5 litres) of water during every hour of operation. While many high efficiency units have condensate directed to a nearby floor drain, some condensing furnaces or boilers must utilize a condensate pump sending the liquid to a remote drain elsewhere in the building.

Sometimes the condensate is pumped to a sink, laundry tub, or even outside. Pumping condensate to a receptacle that can be stopped-up is inviting a flood creating property damage. All condensate pumps should have a secondary float switch dry contact wired into the appliance control circuit shutting it down in the event of a condensate pump failure. Note: always interrupt the “R” circuit. When using a three- or four-wire communication system, the data links must not be wired through an external switch or relay contact.

Overflowing evaporator drain pans used with furnace coils, air handler coils, mini splits, even dehumidifiers create lots of insurance claims. More often than not, the mini-flood results from lack of annual preventive maintenance: dirty coils, plugged drain lines, loss of charge mean lots of water with nowhere beneficial to go. It is common to see humidifier, evaporator coil and furnace condensate drainage all piped into one undersized soft plastic drain pipe that could easily be pinched off. It is better to have a licensed plumber install a trapped standpipe to collect pumped condensate than risk a minor flood caused by improper drainage materials and techniques.

Furnaces, water heaters, boilers and air handlers should be installed on a solid concrete base raising the appliance about two inches above the floor (50 mm.) providing some protection from minor flooding. Install a float switch in the evaporator coil secondary drain outlet. Use drain pan treatment tablets in the evaporator coil and condensate pump. Blow out the drain lines on every maintenance call. Do not reduce the manufacturer provided drain outlets and use PVC pipe to prevent crushing and pinching.

Several manufacturers have water control and flood warning devices available if your business includes installing IoT devices. Two pole moisture detectors placed near the water heater, furnace or boiler are shorted-out by water on the floor sending a signal to sound an alarm or even to operate a water valve shutting off the water supply. The homeowner receives a text message or e-mail advising that the system has been activated. Your company could receive the alarm message as well.

I have no answers for Mother Nature’s wrath; destructive overland flooding is a fact of life. However, on the HVAC side, it is important that we do all we can to prevent as much water damage as possible by using standard industry techniques and materials, by providing protective devices wherever available and by encouraging equipment owners to better maintain their HVAC systems.

Ian McTeer is an HVAC consultant with 35 years experience in the industry. He was most recently a field rep for Trane Canada DSO. McTeer is a refrigeration mechanic and Class 1 Gas technician.

FOR POINTERS ON HOW TO PREVENT MINOR FLOODING CLICK HERE.